| Inflation Reports In December, the Bureau of Labor Statistics (BLS) released the latest reports on CPI and PPI. The CPI news release on December 10, 2021, stated “The all items index rose 6.8 percent for the 12 months ending November, the largest 12-month increase since the period ending June 1982.” Additionally, it stated “The monthly all items seasonally adjusted increase was the result of broad increases in most component indexes, similar to last month. The indexes for gasoline, shelter, food, used cars and trucks, and new vehicles were among the larger contributors.” |

| Then, on December 14, the PPI news release stated, “On an unadjusted basis, the final demand index rose 9.6 percent for the 12 months ended in November, the largest advance since 12-month data were first calculated in November 2010.” Basically, this is telling us what we already suspected: Inflation is running at the highest levels in several decades. Federal Reserve On December 14-15, the Federal Open Market Committee of the Federal Reserve met. They began their prepared statement with “The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.”Additionally, “Supply and demand imbalances related to the pandemic and the reopening of the economy have continued to contribute to elevated levels of inflation. Overall financial conditions remain accommodative, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.” Further, “The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent.” Then the Committee stated “In light of inflation developments and the further improvement in the labor market, the Committee decided to reduce the monthly pace of its net asset purchases by $20 billion for Treasury securities and $10 billion for agency mortgage-backed securities. Beginning in January, the Committee will increase its holdings of Treasury securities by at least $40 billion per month and of agency mortgage‑backed securities by at least $20 billion per month. The Committee judges that similar reductions in the pace of net asset purchases will likely be appropriate each month, but it is prepared to adjust the pace of purchases if warranted by changes in the economic outlook.” So, the Committee acknowledges that inflation has been running well above their long run target range, but they have decided not to change short-term interest rates just yet. Instead, they will accelerate their tapering of Quantitative Easing (QE). The financial markets currently anticipate approximately three increases to short-term rates during 2022. So, it looks to me like they want to decrease their bond purchases first and then start increasing rates. |

| My Assessment In my opinion, the Fed is in a Trap. Here is why: One, the closure and re-opening of the economy, as well as some drastic weather events have caused some very large imbalances between supply and demand. Imbalances like these definitely cause price inflation. They can also cause price deflation. But those price adjustments tend to influence actions in the economy that remove these imbalances and the resulting price changes smooth out over time. However, there is another type of inflation at work here and that is monetary inflation. When the supply of money in the system increases faster than the value of the goods and services in the economy, then the value of those goods and services will increase when measured in those monetary units, e.g., USD. This doesn’t always show up as price inflation. Often it can show up in asset value inflation. When the Federal Reserve started QE in 2009, they didn’t call it QE1 because they thought it was temporary. It has become more or less permanent over the last 12 years. One can easily argue that all the QE from 2009-2021 is what has continually driven up the stock market, the bond market, the real estate market, and everywhere that people with some wealth would invest or store their money. The value of bonds going up drives interest rates down and we’ve all seen how low interest rates have been for many years now. Low interest rates lead to increased investment due to a low cost of capital which then leads to increases in prices of investable assets like real estate and businesses. Low interest rates also make it very cheap for the government to borrow and spend to stimulate the economy. |

| The Fed Trap But here is the trap…if the Fed stops QE, that stops the ongoing injection of money into the system and interest rates will begin to rise (i.e., lower demand for bonds = bond prices drop = interest rates rise). If the Fed also increases short-term rates, we will see the cost of capital and interest go up all across the yield curve. |

| For the Federal Government, the biggest debtor in the world, this will significantly increase their cost of servicing the debt. The government will either have to significantly raise tax rates, which they don’t like to do in an election year, or the Fed will have to buy more treasuries from the government so that they can pay the interest. Buying more treasuries puts the Fed back into the mode of increasing the money supply which takes us back to more monetary inflation. So the trap is either keep interest rates low which means they will have to keep up QE (and continue to increase the money supply) or let interest rates rise which will likely lead to QE to fund higher interest on debt service (which leads back to an increase in the money supply). These actions impact us but we can’t control them. So, what does all of this mean for you and me? What can we control? |

| Wealth Preservation To me, wealth preservation is a top priority with any investment. But it’s more than that. Today, I’ll focus on a basic question. What is Wealth? In the dictionary, most definitions are some form of a store of money, valuable possessions, property, or other riches. I think of Wealth as the accumulated value of all our hard work. The assets that represent our wealth should maintain or hold their value over time, or store value. Over the millennia, wealthy people, or families, have stored their wealth in certain types of assets, such as precious metals, land, natural resources, and sometimes fine art or collectibles. Why have they chosen these types of assets? I think these assets all have certain characteristics in common related to economic value. They all have a certain level of demand over time due to their utility to human life. They all also generally have a limited supply that cannot easily be changed over time. These types of assets are all “Real” in a sense that they are not represented by paper claims, such as stocks, bonds, options, mutual funds, or currency. How is Wealth Stolen or Destroyed? Wealth is generally destroyed or taken from us through the following means: Taxes by governments. This is a direct taking of wealth. I’m not saying this is a bad thing, just that it represents an outside entity exerting control over our own financial security. Inflation of the currency. If wealth is stored in currency that is being expanded through printing of more currency then that currency will not store the value of wealth.Storage (investment) in assets that do not maintain their value; what I call paper assets. The value of paper assets can easily be manipulated by others. |

|

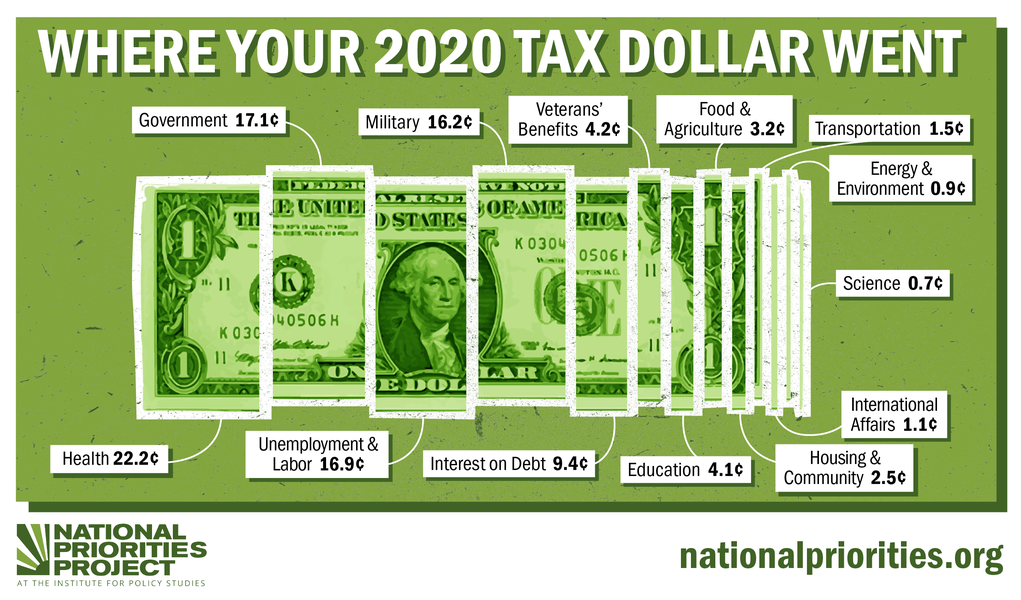

| Purpose of the Tax Code As I have written in my special report on the differences between investing in Main Street vs Wall Street, I discuss the purpose of the tax code. Most people think that everyone must pay a certain level of taxes. That is not true and you can tell by the way the tax code is written. The U.S. tax code is roughly 7000-8000 pages of text. Only about 1% of this text, or less, tells us how much tax must be paid. However, the rest (over 99% of the text) tells how to get back what we paid. These are called financial incentives. The government adds, removes and tweaks these incentives over time to change the behavior of its citizens. There are so many incentives that it is possible to not be required to pay any taxes legally. |

|

| Loop-holes? Many people believe that these financial incentives are loop-holes in the tax code. I think you can only call them a loop-hole if they are accidental. If a loop-hole existed, I would think the government would quickly remove them as soon as they were discovered by the IRS. But, the vast majority of these big financial incentives in the tax code have been around for decades and the government continues to support them. Why?I believe that there is a general belief across a population of citizens that if someone becomes very wealthy, they need to give back to society such that society benefits in a valuable and charitable way. I think the tax code supports this concept. I think the tax code basically gives you two options to give back to society. One, you can pay a certain percentage of your income or wealth to the government and let the government spend that money in ways that benefit society.Or two, you can follow the financial incentives in the tax code and invest your money in ways that either 1) create jobs, 2) provide places for people to live or conduct business, 3) provide energy to the economy (because nothing works without some form of energy), or 4) help people in a less fortunate situation. These all benefit society greatly and are supported through financial incentives in the tax code. |

| Passive Cash Flow GenerationWe don’t live off savings, we live off cash flow. Investments that produce cash flow from an early point in the investment cycle are lower risk than those that need appreciation to achieve desired returns. At Match Real Asset Partners, we focus on investing in real assets that produce cash flow. If you don’t need the cash flow, my advice is to continually reinvest (the cash flow) in other real assets that also produce cash flow. Cash flow created on the front-end of the investment is more reliable than appreciation that relies on markets to create. |

|

| Syndications In 2021, we placed $1.4 million of passive investor capital in some carbon capture and sequestration equipment. Based on leverage and current tax regulations, those investors are getting $2.8 million of tax depreciation in 2021 that can be used to reduce any type of active taxable income, including W-2 income. Based on feedback from my investors, they are saving over $800,000 in taxes in 2021 which means they are very quickly getting approximately 55-60% of their investment back within the first year. The total cash flow for all the investors will be $140,000 per quarter. With this cash flow, these investors will have all of their investment back in approximately one year and then continue to experience this cash flow for six additional years. At Match Real Asset Partners, we expect to be able to offer this opportunity to invest alongside us again in 2022. |

|

| Another area we are doing a lot of research is mining of crypto-currencies. There are several potential investment opportunities in this space, including the data center building and operation to host the crypto mining equipment (a real estate play), mining for cryptocurrencies and immediately converting to cash (a cash flow play), and mining for cryptocurrencies and holding the cryptocurrency as an inflation hedge (a wealth protection play). Other areas that Match Real Asset Partners is researching opportunities to invest in 2022 include oil & gas production, residential housing and rural undeveloped land. As other investment opportunities are developed and made available to investors, we will discuss those in these monthly newsletters. If you have any questions about the content or interest in learning more about our investment opportunities, I would love to talk to you. Click here to schedule a call. |

Match Real Asset Partners LLC is an investment syndication company with a goal to partner with successful operators to provide private placement investments in assets that are expected to provide passive cash flow while protecting wealth and reducing taxes.

Simply fill out the form below to receive valuable news and annoucements directly to your inbox!